Dec 13 - Welcome to the home for real-time coverage of markets brought to you by Reuters reporters. You can share your thoughts with us at markets.research@thomsonreuters.com

BETTER IN THE MIDDLE… BETWEEN BULLS AND BEARS (1231 GMT)

Staying in the middle between bullish and bearish equity views might be the right choice as uncertainty is bound to remain high, at least for a while.

Register now for FREE unlimited access to reuters.com

Cyclical stocks underperformed recently on concerns about the economy due to the Omicron variant, while tech companies came under pressure due to interest rate hike fears.

Such moves were consistent with short-term bond yields rising -- as markets are pricing in more Fed rate hikes -- while long-term rates were falling due to a risk-off environment.

But, the flattening of the curve was “exacerbated by hedge funds that had bet heavily on a steeper curve and now had to reduce this position,” Berenberg analysts say.

So, we shouldn’t be too pessimistic about possible risk-off moves by investors.

Berenberg flags that optimists “believe in double-digit equity returns with no disruption”, and the “pessimists expect a sharper correction due to tighter Fed policy.”

“The truth lies in the middle,” they argue.

The chart shows the spread between 2-year and 10-year U.S. bond yields, which tightened recently.

(Stefano Rebaudo)

*****

DON'T LET VOLATILITY RUIN A GOOD NARRATIVE (1142 GMT)

While most analysts expect 2022 to be another good year for equities, and particularly European stocks, the murky visibility for the next few weeks is definitely an issue.

There's indeed a combo of inflation and pandemic worries in the way of an otherwise bright outlook for corporate profits.

"This environment is clearly different from 2021 and may lead to higher equity-market volatility over the next few months, as uncertainty surrounding high inflation rates and central banks’ monetary policy response is likely to persist", Unicredit analysts wrote in their 2022/23 outlook.

"Additionally, the emergence of the Omicron variant of COVID-19 serves as a sobering reminder that the headwinds generated by the coronavirus pandemic have not completely gone away", they add while they pencil a 10% rise for European stocks.

Overall the picture isn't that bad.

"We expect company earnings to continue to rise in 2022, although at lower momentum as economic growth has peaked globally and as supply-chain bottlenecks as well as high energy and commodity prices continue to constrain earnings".

Tactically, they believe defensive stocks, which are less affected by current supply-chain problems, to fare better, particularly in sectors such as Food & Beverage, Consumer Products & Services, Health Care and Technology.

They're also upbeat for banks which should benefit from rising yields and are typically seen as a good inflation edge.

(Julien Ponthus)

*****

MINERS GET CHINA BOOST (0859 GMT)

As expected, European shares are off to a positive start, with cyclicals leading the way at the expense of defensives, suggesting relative calm ahead of a wave of hawkish signals by central banks this week to fight rising price pressures.

Stand-out gainers are miners (.SXPP), up 1.7%, with the sector benefiting from the risk-on attitude but also getting an extra lift from talk China could boost fiscal stimulus, which also helped metal prices rally. read more

China on Friday said it would implement a prudent monetary policy and a proactive fiscal policy to stabilise the economy and keep growth within a reasonable range in 2022. read more

Rate sensitive banks (.SX7P) were also in demand, up 0.6%, along with travel (.SXTP), autos (.SXAP) tech (.SX8P), and oil (.SXEP) stocks.

M&A also provided support with Vifor (VIFN.S), shooting up 14% to the top of the STOXX after the Swiss drugmaker confirmed talks with Australia's CSL about a possible transaction.

(Danilo Masoni)

*****

GEARING UP FOR CENTRAL BANK ACTION (0747 GMT)

After recovering quickly from the Omicron scare, equity markets look set to kick off a busy week for central banks on the front foot.

With some hawkish signals expected, markets could be in for a bout of volatility in the closing days of 2021 even though some of the policy shifts, particularly by the U.S. Federal Reserve have been well-telegraphed in advance, leaving investors somewhat prepared.

European stock futures are in the black after gains in Asia, and U.S. futures also point north after the S&P 500 clocked its 67th closing record high of the year on Friday and investors started watching for Apple (AAPL.O) becoming the first $3 trillion company.

But it's not just about U.S. policy this week. Interest rate hikes are in store for a raft of central banks in emerging markets from Russia to Mexico, and then there's also the European Central Bank and the Bank of England.

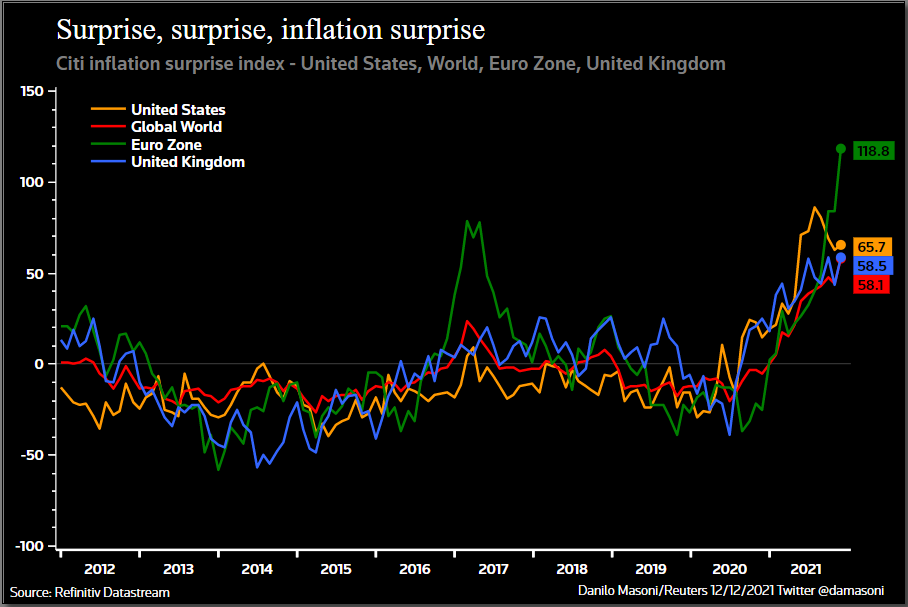

So while inflation surprises haven't stopped the equity bull run - as firms have been able to pass on to consumers rising costs and corporate margins have reached record highs - they have stepped up the pace of rate hikes globally.

There have been 59 rate hikes across investable markets so far this year with a cumulative net increase of 2,570 basis points, according to central bank data collected by financial services firm Black Cuillin.

Also, in the U.S., moderate democrats are becoming increasingly worried about the political fallout of high prices and are pushing for more aggressive policy tightening, according to the Financial Times.

Reflecting bets of early 2022 rate hikes after U.S. inflation rose to the strongest reading since 1982, 10-year U.S. Treasury yields edged up towards the psychological 1.5% mark.

Elsewhere, the pound was set for a beating after PM Johnson warned of Omicron "tidal wave", while oil prices extended their rally, suggesting little worry about the variant.

Key developments that should provide more direction to markets on Monday:

- Chinese artificial intelligence start-up SenseTime Group postponed its $767 million Hong Kong IPO after being placed on a U.S. investment blacklist [USN:L1N2SY02Y]

- Credit Suisse announced a wide-ranging overhaul of its executive board as the Swiss bank seeks to move on from a horrendous year where it has been battered by a stream of controversies and losses [USN:L8N2SY0LD]

- Australian biopharmaceutical giant CSL confirmed it is in talks to buy Swiss drugmaker Vifor Pharma in a deal reported by media to be worth about A$10 billion [USN:L4N2SX0XB]

- German wholesale price index

- BOE Financial stability report 1700 GMT

- France's Macron attends summit of four Visegrad countries Poland, Hungary, Czech and Slovakia

- Canadian Finance Minister Chrystia Freeland and Bank of Canada Governor Tiff Macklem hold presser on 5-year monetary policy framework

(Danilo Masoni)

*****

EUROPE: STOCK FUTURES ON THE UP (0730 GMT)

European shares are set to open higher today as investors prepare for a raft of central bank meetings this week that could tighten monetary policy further in the face of rising inflation.

Following gains across Asian markets, Euro STOXX 50 futures were pointing north, and were up 0.3%, while derivatives on U.S. stock indexes were also rising by around the same amount following a record closing high on Friday.

(Danilo Masoni)

*****

Register now for FREE unlimited access to reuters.com

Our Standards: The Thomson Reuters Trust Principles.

"between" - Google News

December 13, 2021 at 07:31PM

https://ift.tt/3pVhtvs

LIVE MARKETS Better in the middle... between bulls and bears - Reuters

"between" - Google News

https://ift.tt/2WkNqP8

https://ift.tt/2WkjZfX

Bagikan Berita Ini

Related Posts :

Negotiations on schedule between city and PT mill - Port Townsend Leader

Negotiations on schedule between city and PT mill - Port Townsend Leader- My 911 Call: An Adventure at Lunchtime Between Myself, My Alter Ego & the Police - Dan's Papers

- Supreme Court Turns Down Appeal in Clash Between Florist and Gay Couple - The New York Times

- Jewelry store fight between brothers turned deadly, report states - Gilroy Dispatch

- SR 14 preservation work between Wood Creek and Alderdale Road in Klickitat County begins next week - Access Washington

0 Response to "LIVE MARKETS Better in the middle... between bulls and bears - Reuters"

Post a Comment